From Duff To Chuffed – Housing Boom On The Way

Glenigan is predicting an absolute boom in construction over the next two years, particularly residential, following a bit of a duff 2025. Revised...

Read Full Article.gif)

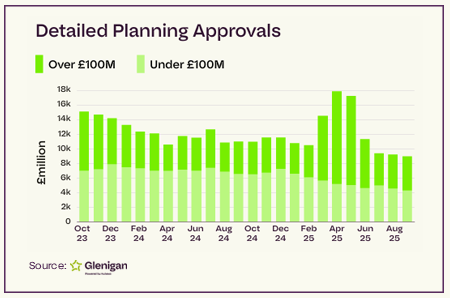

The latest Glenigan Review shows UK construction activity continuing to fall against a backdrop of economic uncertainty. Project starts have declined by 15% during the review while planning approvals have nosedived -21%.

The review focuses on the three months to the end of September 2025, covering all major (>£100m) and underlying (<£100m) projects, with all underlying figures seasonally adjusted.

All fall down

Once again, Glenigan’s October Review paints a picture of a sector continuing to slow down, as investor confidence fails to return to the private market and many public projects face significant delays. It was a case of across-the-board decline with project starts, main contract awards and detail planning approvals all down compared to both the preceding three months, and the same period last year.

Looking at the former, project starts fell by 15% against the previous quarter and plummeted to a shocking 40% on 2024 levels.

Likewise, the value of planning approvals was slashed by approximately a fifth (-21%) during Q.3 and when measured against the previous year (-18%). Whilst main contract awards only dipped a modest 2% compared to the preceding three months, they finished almost a third down (-32%) against the previous year.

The perfect storm

Commenting on the results, Yuliana Ivanykovych, a senior economist at Glenigan says: “The situation seems to be getting worse as the year progresses and at this rate something truly transformative will need to happen to kick-start activity. Activity is depressed across both underlying and major projects, a result of low business confidence and the slow progress of government funded projects.

Couple that with the industry’s long-term labour market challenges, wafer-thin margins and growing concerns over rising costs and you have a perfect storm, which the industry will have to try and weather in the months to come.”

Budget on the horizon

Ivanykovych continues, “Not only that, there is added caution ahead of the Budget. Investors are keen to keep their powder dry, whilst government departments cautiously watch for any changes to their funding allocations which might put capital projects at risk.”

Residential continues to fall

The residential sector is in decline, with that positive growth spurt seen over the spring/summer now seeming a distant memory.

Private housing experienced a particularly poor period whilst social housing has been left with a significantly weakened pipeline. Even though there was strong growth in major project starts within this vertical, compared to both last year and the previous quarter, it was not quite enough to pull it up into positive figures.

Regionally, performance was generally weak, with most posting lower project starts compared to Q.2 and the previous year. However, London and the South East both registered small project start increases, up 8% and 2% respectively on 2024. The latter also experience an uptick in planning approvals, growing 10% year-on-year, with the East of England (+28%) and South West (+11%) posting increases on a year ago.

High-rise for office starts

Offices continued their moment in the sun, despite planning approvals falling by three-quarters (-76%) and main contract awards down by 9% compared to 2024, the vertical posted an impressive 82% increase in starts year-on-year. This boost can be predominantly attributed to a spike in underlying starts as well as policy-driven momentum, with the government recently signing a Tech Prosperity Deal, which has led to announcing an AI ‘growth zone’ in the North-East.

This £30bn investment will make the region home to one of the largest data centre hubs in Europe and hint at how this type of building will likely keep performance relatively resilient in the office vertical (which includes data centres) in the months and years to come.

Picture: The latest Glenigan Review shows UK housebuilding falling.

Article written by Cathryn Ellis

16th October 2025